🇺🇸 🇨🇳 Is the U.S. fueling its competitors’ rise by exporting cheap ethane—and in the process, giving away its shale gas advantage to the world?

- Dec 18, 2025

- 1 min read

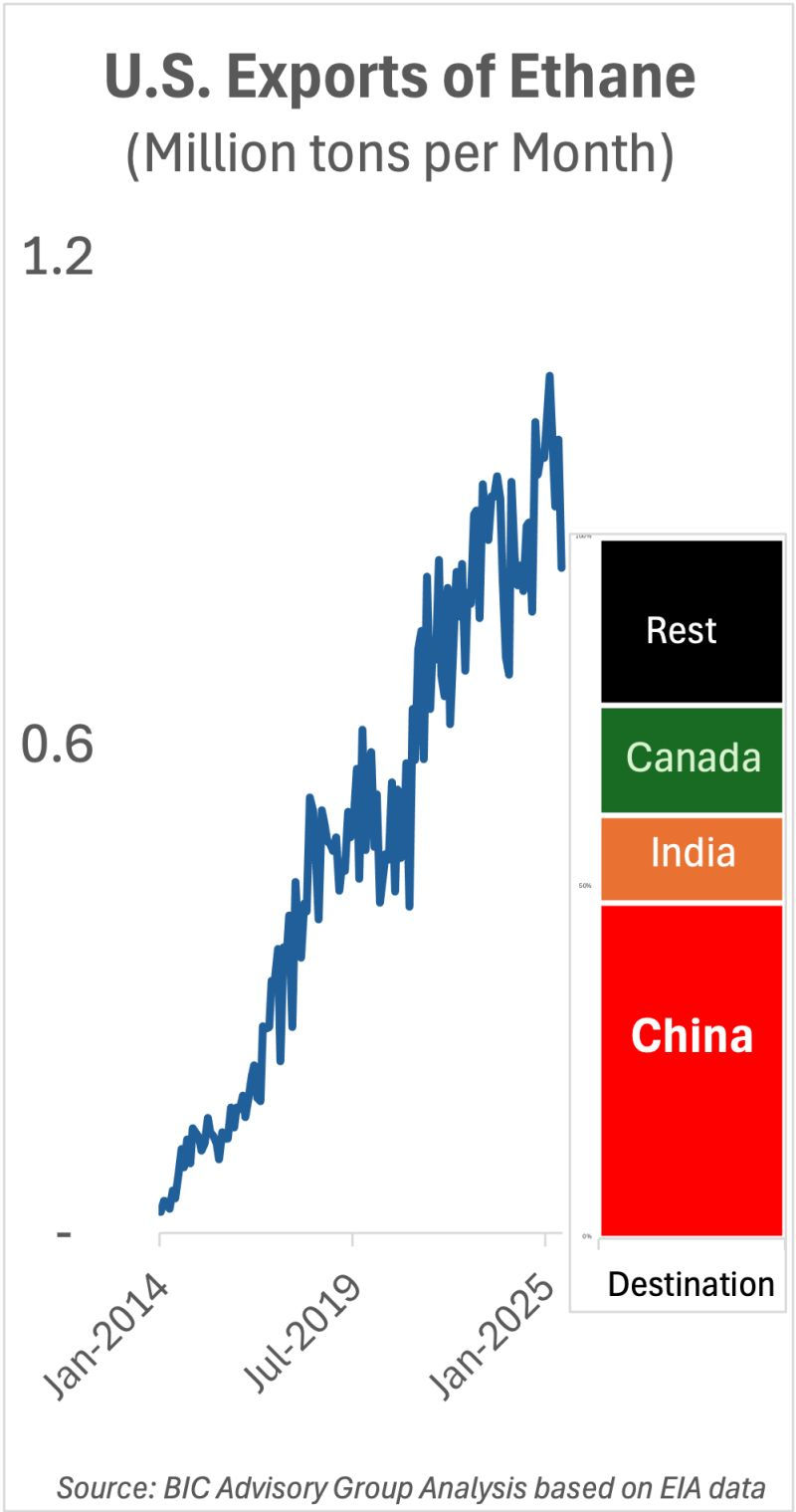

The chart above shows how U.S. ethane exports have surged from zero just over a decade ago to nearly 10 million tons per year today—with volumes increasingly flowing to America’s fiercest trade rivals overseas.

At BIC Advisory Group, we’ve been analyzing what this means for U.S. competitiveness. The key questions:

👉 Is this smart monetization of surplus shale gas?

👉 Or a “cash now, regret later” strategy?

Here’s what our analysis shows:

This export boom wasn’t crafted as U.S. industrial policy. It was Adam Smith’s invisible hand—billions invested in terminals, vessels, and infrastructure by private capital chasing attractive returns.

By exporting ethane, the U.S. is effectively handing competitors a low-cost feedstock to produce ethylene and polyethylene—the very chemicals U.S. producers also export.

Yet, even at today’s levels, US ethane exports represent <5% of global ethylene capacity. And with ~50% of the world’s crackers still tied to more expensive oil-based feedstocks, polyethylene pricing remains anchored to oil, not ethane.

The takeaway from BIC Advisory Group: for now, the U.S. gets to have it both ways: profiting from ethane and derivative exports.

But the chart also tells another story: this game has limits. The piper will come knocking. Just not today—or tomorrow.

Welcome news for major US PE exports: ExxonMobil, Dow, Chevron Phillips Chemical Company, LyondellBasell, Shell, Formosa Plastics Corporation, U.S.A., NOVA Chemicals, Montachem International, Inc., Tricon Energy, Ravago and Vinmar International

Comments